Wool continues to hold a unique position in the global textile industry: a traditional fiber navigating a modern, sustainability-driven market.

Today, the international wool trade reflects a highly structured ecosystem, where a small number of exporting countries supply raw materials to powerful industrial economies. While its overall share of global trade remains limited, wool has maintained its importance thanks to its premium quality, versatility, and environmental appeal.

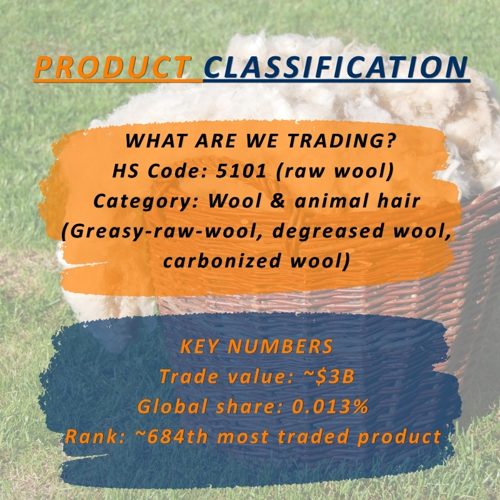

PRODUCT CLASSIFICATION

In global trade systems, wool is classified under the Harmonized System (HS) code 5101, referring to “wool, not carded or combed”, the raw material before industrial treatment and transformation.

This category falls within the broader “Wool & animal hair” sector and includes different early-stage forms of wool:

• Greasy wool (raw and untreated)

• Degreased wool (partially cleaned)

• Carbonized wool (processed to remove impurities)

• Other non-combed wool types

Despite its long-standing relevance, wool represents a very small share of global trade, accounting for roughly 0.013% of total traded goods worldwide, with an overall value close to $3 billion annually in recent years.

This limited share highlights a key characteristic of wool; it is not a mass-market commodity, but rather a specialized raw material, primarily used in high-quality textiles and niche applications.

Additionally, the product shows a relatively low complexity at the raw stage (PCI around -1.33), meaning its value chain becomes more sophisticated only after processing into yarns, fabrics, and garments.

EXPORT

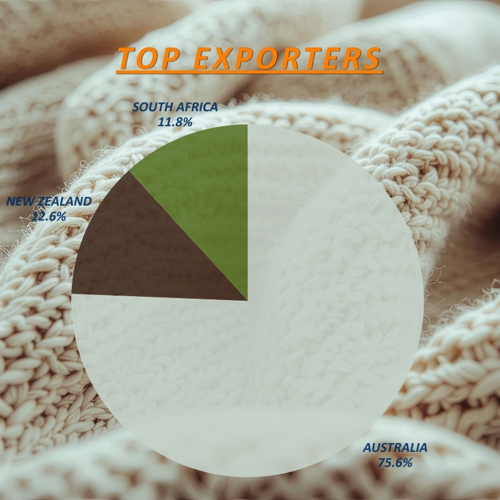

The global export landscape for wool remains highly concentrated and geographically specialized.

A small group of countries continues to dominate global supply, with:

• Australia leading by a wide margin, with exports exceeding $1.8 billion annually

• New Zealand contributing roughly $250–300 million

• South Africa close behind with similar export volumes

Australia’s dominance is particularly striking. Thanks to its strong sheep farming industry and leadership in fine Merino wool, it consistently accounts for a major share of global export value, often exceeding 50% and, in some estimates, approaching 60%.

This concentration reflects structural advantages:

• Favorable climate and large grazing areas

• Advanced farming and production techniques

• Strong integration with global textile supply chains

At the same time, the wool export market has been experiencing moderate downward pressure in recent years, with global trade values showing a gradual decline, including a recent contraction of around -5% year-on-year.

This trend is linked to several structural shifts:

• Increasing competition from synthetic fibers

• Changes in consumer preferences

• Volatility in global textile demand

Despite this, wool retains a competitive edge in premium and sustainable segments, where quality often outweighs cost considerations.

IMPORT

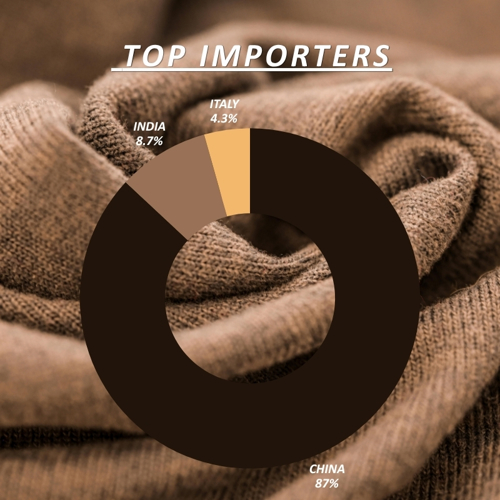

On the demand side, wool trade is even more concentrated, driven by industrial processing needs rather than raw material availability.

The import landscape is led by:

• China, with purchases exceeding $2 billion annually

• India, around $200 million

• Italy, approximately $100–120 million

China plays a central and strategic role, consistently absorbing the largest share of global wool imports, historically accounting for close to two-thirds of total demand.

Its dominance is explained by its position as:

• The world’s largest textile manufacturing hub

• A major processor of raw wool into yarns, fabrics, and finished goods

Other importing countries contribute in more specialized ways:

• India supports large-scale textile production for both domestic and export markets

• Italy focuses on high-end fashion and luxury wool products, reinforcing Europe’s role in premium manufacturing

Overall, the global wool trade follows a clear and persistent pattern:

Raw wool flows from agricultural exporters to industrial processors, where it is transformed into higher-value textile products.

CURIOSITY CORNER

Beyond trade flows, wool stands out as a remarkable natural material, with characteristics that explain its continued relevance.

A small but valuable fiber

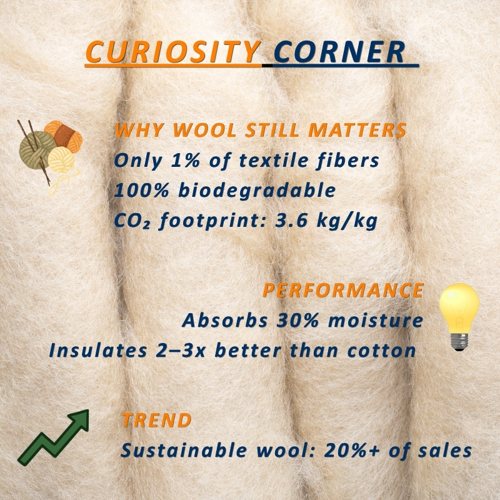

• Wool accounts for only about 1% of global textile fibers by volume, making it a niche material in a market dominated by synthetics.

Strong sustainability credentials

• It is 100% biodegradable, decomposing in a matter of months and naturally enriching the soil

• Its carbon footprint (around 3.6 kg CO₂ per kg) is lower than many synthetic alternatives

High-performance natural fiber

• Wool can absorb up to 30% of its own weight in moisture without losing comfort

• It offers insulation levels 2–3 times higher than cotton, making it ideal for technical and outdoor apparel

Rising demand for eco-friendly materials

• Sustainable wool products now represent over 20% of global wool apparel sales, reflecting a steady increase in environmentally conscious consumption

Production remains geographically concentrated

• A limited number of countries (particularly Australia, China, and New Zealand) continue to dominate global production, reinforcing supply chain concentration.

CONCLUSION

The global wool market is a clear example of a concentrated, high-value supply chain, where geography and specialization play a central role.

• A few exporting countries dominate the supply of raw wool

• A small number of industrial economies drive global demand

• The overall trade remains relatively small (around 0.013% of world trade) but strategically important

Although recent years have seen moderate declines in trade volumes, the long-term outlook is shaped by stronger structural trends:

• Increasing focus on sustainable and natural fibers

• Growth in premium and luxury textile segments

• Renewed interest in durable, high-performance materials

In this context, wool continues to stand out as a timeless yet evolving resource. Its ability to combine tradition, performance, and sustainability ensures that, even in a rapidly changing textile industry, it remains a relevant and valuable global commodity.